If you’re searching “create offshore company”, you’re probably trying to achieve one of three things: protect assets, structure an international business, or simplify cross-border ownership (property, shares, IP, investments). The catch is that “offshore” is no longer a shortcut. Today, the fastest offshore setups are the ones built to pass banking, due diligence, and ongoing compliance from day one.

This guide walks you through an offshore formation process that is:

- banking-ready (so you don’t get stuck after incorporation),

- compliance-first (so the structure holds up long-term),

- purpose-led (so you choose the right jurisdiction and entity type the first time).

If you want your structure mapped to your goals (and your personal tax/residency reality), First Elite Global can build a clear plan in one call and manage the entire setup end-to-end.

What “Offshore Company” Really Means (And What It Doesn’t)

An offshore company is typically a legal entity incorporated in a jurisdiction different from where the owners live or where the business is primarily managed.

Offshore doesn’t automatically mean:

- anonymous,

- tax-free everywhere,

- “no reporting”,

- faster banking.

In practice, most reputable jurisdictions now require:

- clear ownership records,

- strong identity checks (KYC),

- documented source of funds/wealth (especially for banking),

- ongoing filings or renewals.

Bottom line: offshore can be a legitimate tool, but only when it’s built for transparency, reporting, and real-world operations.

Should You Create an Offshore Company? Use This 60-Second Fit Check

Offshore often makes sense when you need:

- Holding structures: owning shares in other companies, or holding investments

- Asset ownership: property, yachts, trademarks, domains, IP

- International contracting: invoicing outside a specific local market

- Group structuring: separating risk, isolating assets, simplifying ownership

- Cross-border expansion: managing vendors/clients across multiple countries

Offshore is usually the wrong tool when you need:

- local trading in a country that requires a local licence/office,

- investor visas tied to an onshore licence,

- venture capital readiness (many VCs prefer onshore, audited, substance-backed entities),

- payroll, staff hiring, or premises in the target country.

If you’re unsure, the simplest next step is a short consultation where we map your goals to the right structure and jurisdiction—before you spend money on the wrong setup.

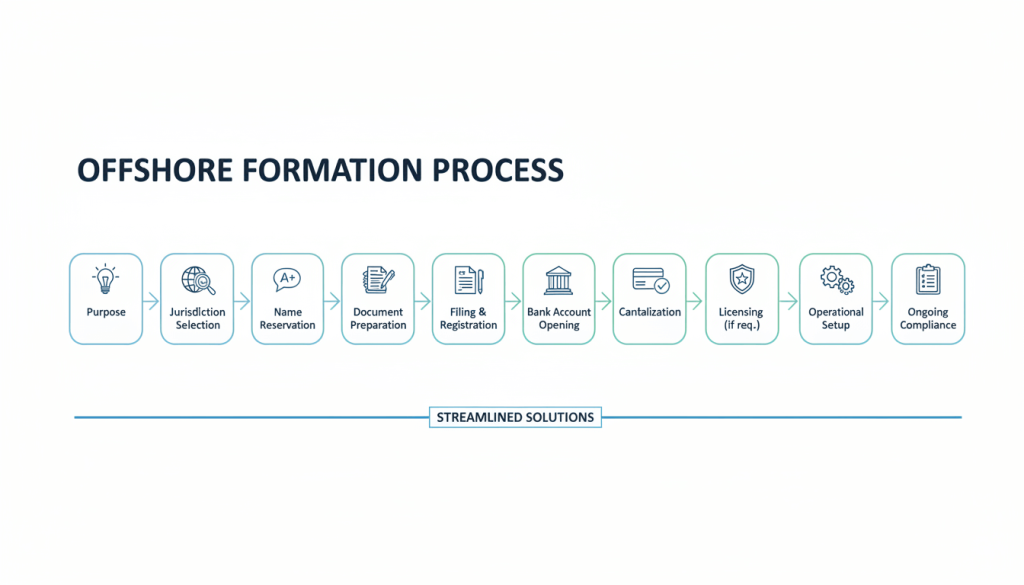

Offshore Setup Steps (Overview)

Here’s the offshore incorporation guide in one view:

- Define your exact use case

- Map your compliance perimeter (tax, reporting, banking)

- Shortlist jurisdictions using a scorecard

- Choose the entity type and ownership model

- Prepare a “banking-ready” KYC + source-of-funds file

- Incorporate (name, agent, constitutional docs, registers)

- Complete post-incorporation documents (resolutions, UBO register, share certificates)

- Open banking and payment rails

- Set up ongoing compliance (accounting, renewals, substance, recordkeeping)

- Review annually as your situation changes

Now let’s do it properly—step by step.

Step 1: Get Crystal Clear on the Purpose (This Prevents 80% of Mistakes)

Write one sentence that starts with:

“I want to create an offshore company to…”

Examples:

- “…hold shares in my operating companies and ring-fence liability.”

- “…own and manage a property portfolio across countries.”

- “…invoice international clients while keeping operations outside a local market.”

- “…hold IP and license it to operating subsidiaries.”

This purpose statement determines:

- which jurisdictions fit,

- whether you need substance,

- what banks will ask for,

- whether an offshore company is even the right tool.

Step 2: Map Your Compliance Perimeter (Before You Pick a Jurisdiction)

This is where most online guides go wrong: they start with “best jurisdictions” instead of starting with your reality.

You need to understand:

- Where you are tax resident (and any reporting obligations that follow you)

- Where the company is managed and controlled (board decisions, directors, signatories)

- Whether your home country has CFC rules (controlled foreign company rules)

- Whether you need audited accounts for banking or counterparties

- Your industry risk rating (crypto, trading, consultancy, payments, advertising, etc.)

If you want a structure that survives real banking and real compliance, this step is non-negotiable.

Step 3: Choose a Jurisdiction Using a Scorecard (Not Hype)

Forget “best offshore jurisdiction” lists. Use a scorecard based on what banks and regulators actually care about.

The 9-Factor Jurisdiction Scorecard

Rate each factor High / Medium / Low for your shortlist:

- Reputation & banking acceptance

- Regulatory clarity (rules you can actually follow)

- Ownership records & transparency (how it’s handled, who can see what)

- Cost to incorporate + renew annually

- Speed & predictability (timelines, not marketing claims)

- Substance expectations (if relevant to your activities)

- Treaty access (if needed and realistically usable)

- Professional ecosystem (agents, accountants, legal support)

- Exit simplicity (can you restructure later without pain?)

Common jurisdiction “buckets” (a useful way to shortlist)

A) International holding-focused jurisdictions

Often chosen for holding shares/assets and group structuring.

B) Trade and operational jurisdictions

Sometimes better if you need real operations, counterparties, or stronger “onshore credibility”.

C) Hybrid approaches

A holding company in one jurisdiction + an operating company elsewhere.

A good setup is rarely “one company, one place, forever.” It’s usually a structure that can scale.

Step 4: Pick the Entity Type (IBC vs LLC vs Holding Co)

Your entity choice affects liability, governance, and banking.

Typical structures you’ll see

- IBC (International Business Company): common in classic offshore jurisdictions; often used for holding and international activity (subject to local rules).

- LLC: flexible management and ownership; can be attractive for certain commercial setups.

- Holding company: sometimes a specific designation; often used as the top entity in a group.

- SPV (Special Purpose Vehicle): created for a single asset or transaction.

Pro tip: Don’t choose the entity because it’s “popular.” Choose it because it matches:

- your purpose statement,

- your compliance perimeter,

- your banking plan.

Step 5: Decide on Ownership and Control (And Don’t Overcomplicate)

Start simple unless complexity is required.

You’ll typically decide:

- shareholder(s),

- director(s),

- ultimate beneficial owner (UBO) disclosures,

- whether you need corporate shareholders (often triggers deeper due diligence),

- who will be the bank signatory.

Banking reality: the more layers you add, the more documentation you’ll need, and the longer onboarding tends to take.

Step 6: Build a Banking-Ready KYC File (The Step Most People Skip)

Incorporation is often the easy part. Banking is where weak structures die.

Create a single folder (PDF format is best) that includes:

Identity & address

- Passport copy (clear, full page)

- Proof of address (recent utility bill/bank statement)

- CV or professional profile (yes, banks ask)

- Personal bank statements (commonly requested)

Business clarity

- One-page business summary (what you do, where clients are, how you get paid)

- Website / online presence (even a basic one helps)

- Contracts or invoices (if you have trading history)

Source of funds / source of wealth

- Sale agreements, dividends, payslips, retained earnings evidence, or other documentation that clearly explains where capital comes from

- A short written explanation that matches the documents (simple and consistent)

This is the difference between “incorporated on paper” and “fully usable structure.”

If you want this handled properly, we’ll prepare a banking-ready file alongside the company formation, so you’re not scrambling afterward.

Step 7: Incorporate (The Offshore Formation Process in Practice)

Once jurisdiction and structure are confirmed, the typical offshore setup steps look like this:

- Name check / reservation

- Registered agent / registered office appointment (where required)

- Prepare constitutional documents (MOA/AOA or equivalent)

- Submit incorporation application + KYC pack

- Receive certificate + registers (company register, directors, shareholders)

- Issue internal documents (share certificates, resolutions, appointments)

What you should receive at the end

- Certificate of incorporation

- Memorandum & Articles (or equivalent)

- Register of directors / shareholders

- Share certificates (if applicable)

- Initial resolutions / appointment letters

- UBO/beneficial ownership records (handled per rules)

Step 8: Post-Incorporation Setup (Make the Company Actually Operable)

This is where professionalism shows up.

Common essentials:

- corporate email domain and basic website

- invoicing template and contract templates

- bookkeeping system (even if light)

- board resolutions for bank account opening

- authorised signatory documentation

- compliance calendar for renewals/filings

Visual idea: a “Day 1 to Day 30 Offshore Launch Checklist” infographic (highly linkable and shareable).

Step 9: Open Banking and Payment Rails (Plan This Early)

Your banking plan should be aligned with:

- jurisdiction reputation,

- business model,

- expected incoming/outgoing volumes,

- client countries,

- compliance expectations.

Practical options to consider

- Traditional corporate bank account (stronger for trade finance, larger volumes)

- Fintech and EMI rails (faster onboarding in some cases, but varies by profile)

- Multi-currency collections (useful for international invoicing)

Important: Don’t incorporate first and “figure out banking later.” Do both as one plan.

If you’d like, First Elite Global can advise on a realistic bank strategy based on your profile and structure—so you choose a route you can actually get approved on.

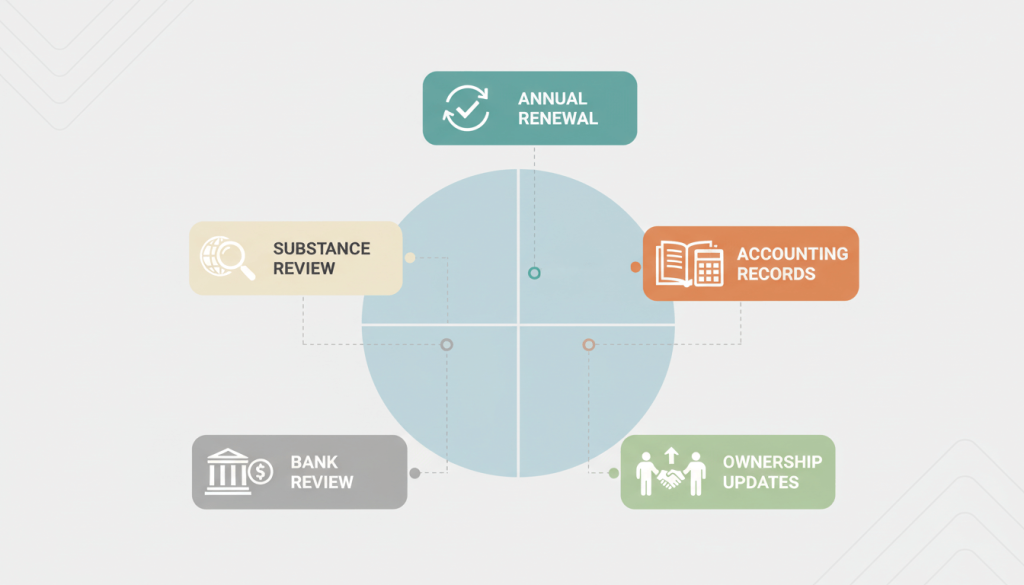

Step 10: Ongoing Compliance (Where Long-Term Offshore Success Lives)

Offshore companies require ongoing maintenance. The exact obligations vary by jurisdiction, but expect some combination of:

- annual renewal fees

- registered agent/office renewals

- annual returns or confirmations (where required)

- maintaining accounting records

- audits (sometimes required, often bank-driven even when not legally mandatory)

- updating ownership/director changes promptly

- substance considerations if you conduct specific activities

The “Keep It Clean” Offshore Compliance Rules

- Keep records organised and consistent

- Don’t mismatch business activity vs what you told the bank

- Avoid unexplained high-risk transactions

- Update documents when your situation changes

- Run an annual review (structure, tax residency, banking needs)

A compliant offshore structure is not a “set and forget.” It’s a system.

A Practical Jurisdiction Decision Matrix (Original, Copy-Paste Friendly)

Use this table to compare options quickly. Fill it in with your shortlist.

| Factor | Option A | Option B | Option C |

| Primary purpose (holding / trade / IP / property) | |||

| Banking acceptance for your profile | |||

| Total first-year cost (setup + support) | |||

| Renewal cost predictability | |||

| Required disclosures (owners/directors) | |||

| Substance expectations (if relevant) | |||

| Speed + predictability | |||

| Ease of adding an operating company later | |||

| Exit or restructure flexibility |

Quick rule: If you can’t confidently fill in “banking acceptance” and “required disclosures,” pause. That’s where most offshore setups fail.

Common Mistakes When People Create an Offshore Company (And How to Avoid Them)

Mistake 1: Choosing a jurisdiction based on “0% tax” headlines

Fix: Start with your purpose and compliance perimeter. Tax outcomes depend on where you live, where management happens, and what the company does.

Mistake 2: Incorporating without a banking plan

Fix: Build the banking-ready KYC pack and bank strategy before you file incorporation.

Mistake 3: Using nominee-style complexity to “hide ownership”

Fix: Modern compliance systems are designed to identify UBOs. Focus on legitimate privacy and proper governance, not concealment.

Mistake 4: Mismatch between declared activity and real transactions

Fix: Keep a clear operating narrative and make sure invoices, counterparties, and payments align.

Mistake 5: Ignoring ongoing obligations

Fix: Create a simple compliance calendar and assign responsibility (you, your accountant, or your service provider).

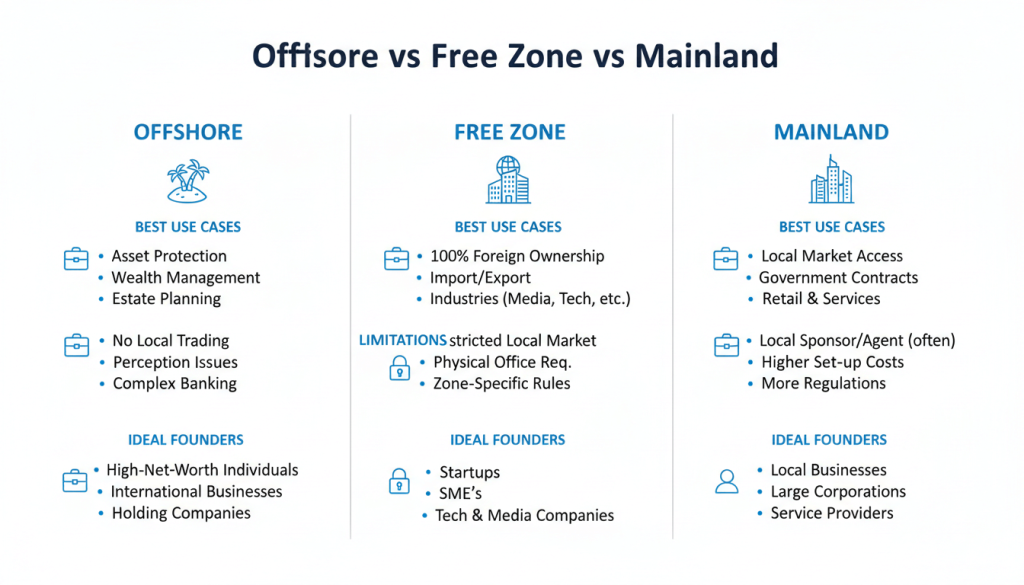

Offshore vs Free Zone vs Mainland (A Simple Way to Choose)

Many founders only realise late that “offshore” isn’t designed for local trading in certain markets.

Use this quick decision guide:

- Offshore: best for international holding/structuring and cross-border ownership

- Free zone: often better for operational businesses, visas, and a clear licensing route

- Mainland: usually best for full local market access, local contracts, and broad commercial flexibility

If your end goal includes visas, premises, or local trading, you’ll likely need an onshore route—even if you keep a separate offshore holding structure above it.

Case-Style Examples (Illustrative, Not Legal Advice)

Example 1: The International Holding Structure

A founder wants to own shares in two operating businesses in different countries. They create an offshore holding company to centralise ownership, simplify shareholder arrangements, and ring-fence risk.

Key success factor: clean governance + clear documentation for banking.

Example 2: The Asset Ownership SPV

An investor wants to hold a single property and keep ownership separate from other ventures. They create a special purpose vehicle (SPV) to isolate liability and make sale/transfer simpler later.

Key success factor: proper recordkeeping and clarity on funding source.

Example 3: The Cross-Border Services Business

A consultant invoices international clients and wants a structure that looks professional, is bankable, and can scale. They build a compliant offshore structure with strong documentation and a clear operating story.

Key success factor: the banking-ready file and consistent transaction pattern.

How First Elite Global Helps You Create the Right Offshore Company

If you want speed, the best shortcut is doing it right the first time.

With First Elite Global, you get:

- a jurisdiction and structure recommendation tied to your goals (not a generic package)

- a banking-ready KYC and source-of-funds file prepared upfront

- end-to-end incorporation handling, including post-incorporation documents

- guidance on the best next step if offshore isn’t the right fit (free zone or mainland alternatives)

If you’re ready to move from research to execution, book a free consultation and we’ll map your structure, timeline, and documentation checklist in one call.

FAQ

1) How long does it take to create an offshore company?

It depends on the jurisdiction, your documents, and how quickly compliance checks are cleared. Incorporation can be quick, but banking and due diligence often take longer than people expect.

2) What documents do I need for offshore company formation?

Most setups require a passport copy, proof of address, and basic background information for each shareholder/director. Banking and enhanced due diligence may require additional documents, including source-of-funds evidence.

3) Is it legal to create an offshore company?

Yes—offshore companies are widely used for legitimate holding, structuring, and cross-border business. The key is to remain compliant with tax, reporting, and anti-money laundering requirements in all relevant countries.

4) Will an offshore company reduce my taxes automatically?

Not automatically. Tax outcomes depend on your personal tax residency, where the company is managed and controlled, what activities it performs, and the rules in each involved country.

5) Can I open a bank account with an offshore company?

Often yes, but approval depends on the jurisdiction, your business model, the clarity of your documentation, and your source of funds/wealth evidence. A banking-ready file significantly improves your chances.

6) Do offshore companies need ongoing compliance and renewals?

Yes. Most require annual renewals, maintenance of corporate records, and sometimes returns or confirmations. Banks may also expect accounting records and ongoing clarity around transactions.