If you run a business in the UAE, the VAT threshold isn’t just a number — it’s a compliance trigger that affects pricing, cash flow, invoicing, and how “investor-ready” your operation looks on paper.

Here’s the core rule most founders need:

- You must register for VAT when your taxable supplies and imports cross AED 375,000 (using the UAE’s rolling time tests).

- You can register voluntarily once you cross AED 187,500 (including certain taxable expenses), even if you’re not required yet.

The details matter because two businesses with the same “sales” can end up with very different VAT obligations depending on what they sell, where customers are, and whether income is taxable, zero-rated, or exempt.

If you want a quick, founder-friendly answer: use the decision checks below, then apply the calculation steps and examples to your own numbers.

Also see: Business licence in Dubai guide

VAT thresholds at a glance

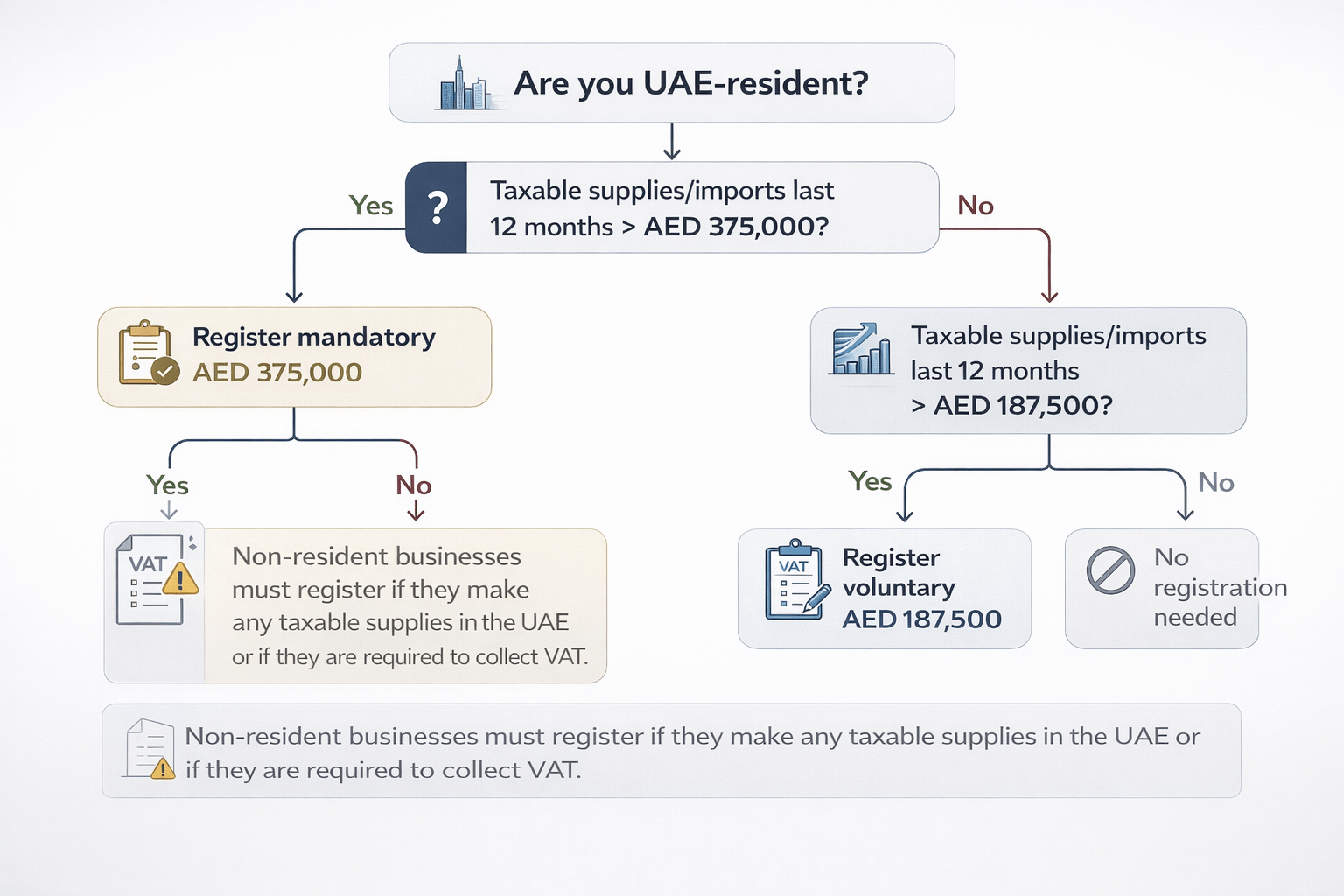

Mandatory VAT registration threshold (AED 375,000)

You are required to register if either of these becomes true:

- Past test: your total taxable supplies and imports exceeded AED 375,000 in the previous 12 months, or

- Forward test: you reasonably expect your taxable supplies and imports to exceed AED 375,000 in the next 30 days

Voluntary VAT registration threshold (AED 187,500)

You may register voluntarily if you are below the mandatory threshold but either of these becomes true:

- Your taxable supplies and imports (or taxable expenses) exceeded AED 187,500 in the previous 12 months, or

- You reasonably expect taxable supplies/imports (or taxable expenses) to exceed AED 187,500 in the next 30 days

Important exception: non-resident businesses

For non-resident businesses making taxable supplies in the UAE, the “AED 375,000 threshold” typically does not apply in the same way — VAT registration can be mandatory even below that figure depending on who is responsible for accounting for VAT on the supply.

What counts towards the VAT threshold (and what doesn’t)

Before you calculate anything, get the definitions right. Many threshold mistakes happen because businesses count all revenue instead of taxable turnover.

Taxable supplies (generally count towards the threshold)

- Standard-rated supplies (VAT charged at the standard rate)

- Zero-rated supplies (VAT charged at 0%, but still “taxable” for threshold purposes in many cases)

- Taxable imports where the treatment would be taxable if supplied in the UAE

Supplies that commonly do not count (or require special care)

- Exempt supplies (these are not taxable supplies)

- Certain “out of scope” items (depending on the nature of the transaction)

If you’re unsure whether your revenue is taxable, zero-rated, or exempt, treat that as a red-flag item and classify it properly before you decide on VAT registration.

Mandatory VAT registration: when you must register

If your business is UAE-resident and your taxable supplies and imports exceed AED 375,000, VAT registration becomes compulsory.

The two tests that trigger mandatory registration

1) The previous-12-months test (rolling)

This is not “calendar year” and not “your financial year” by default. It’s a rolling assessment of the last 12 months.

Founder tip: Put a recurring reminder to review your rolling 12-month taxable turnover every month — the trigger can happen silently while you’re focused on growth.

2) The next-30-days expectation test

If your signed contracts, purchase orders, pipeline certainty, or other evidence shows you will exceed the threshold within the next 30 days, you’re expected to register based on that expectation.

This catches fast-growth businesses early — particularly agencies, consultancies, contractors, and B2B service firms that sign a few large deals in one quarter.

VAT registration deadline: how fast you need to act

When you become required to register, you’re expected to submit your VAT registration application within 30 days of being required to register.

That’s why VAT threshold monitoring should be operational, not occasional. If you realise late, you may still owe VAT from the effective date — even if you didn’t collect it from customers at the time.

Practical consequence: late registration can become an immediate margin hit if you have to pay VAT out of your own pocket on past invoices.

What is the effective date once you cross the mandatory threshold?

In many cases, the VAT registration becomes effective based on when you first became liable (and in some cases the first day of the following month after the month you became required).

This matters because it determines:

- from which date you must charge VAT on taxable supplies,

- what periods you must account for,

- and whether any earlier invoices need correcting (credit notes / adjustments).

If your threshold date is close to month-end or you have mixed invoices (partial payments, milestones), it’s worth mapping the dates carefully.

Voluntary VAT registration: when it makes sense (AED 187,500)

Voluntary VAT registration is not just “nice to have”. For the right business, it can improve cash flow and credibility — and prevent problems when you suddenly land bigger contracts.

When you can register voluntarily

You can register voluntarily once you exceed AED 187,500 in:

- taxable supplies and imports, or

- (in some situations) taxable expenses that meet the criteria

Also see: Company registration in Dubai

Why founders choose voluntary registration

1) To recover input VAT on costs

If you’re spending heavily (rent, fit-out, equipment, software, professional services) and you have VAT invoices, registration may allow you to recover input VAT (subject to rules).

This is common for:

- new offices and fit-outs

- trading businesses building inventory

- marketing-heavy startups

- professional services firms investing in operations

2) To be “procurement ready”

Many established UAE clients (especially in B2B) prefer suppliers who can issue compliant tax invoices and show a TRN. Voluntary registration can remove procurement friction.

3) To avoid a rushed, reactive registration later

If you’re close to the mandatory threshold and growth is predictable, voluntary registration can be a controlled move rather than a last-minute compliance scramble.

When voluntary registration may not be worth it

If most of your sales are to consumers who are price-sensitive, VAT registration may force you to either:

- increase prices (risk conversion), or

- absorb VAT (reduce margins)

Also remember: registration brings ongoing obligations — invoicing standards, return filing deadlines, record keeping, and audit readiness.

Non-resident businesses: the threshold trap

A common misunderstanding: “We’re below AED 375,000 so we don’t need VAT.”

For non-resident businesses making taxable supplies in the UAE, VAT registration can be mandatory even below AED 375,000, depending on whether another party in the UAE is responsible for accounting for the VAT.

This comes up with:

- overseas suppliers selling directly to UAE customers

- foreign consultancies delivering taxable services in the UAE

- cross-border trading arrangements

If you’re not UAE-resident and you sell into the UAE, treat VAT as a first-step compliance review — not a “later” task.

How to calculate taxable turnover for VAT threshold purposes

Use this process to avoid the most common errors.

Step 1: Choose your assessment window

Calculate taxable supplies and imports for:

- the previous 12 months, and

- expected taxable supplies/imports for the next 30 days (if relevant)

Step 2: Add up what counts

Include:

- taxable sales at the standard rate

- zero-rated sales (where applicable)

- taxable imports considered in the registration calculation

Step 3: Exclude what doesn’t count

Exclude:

- exempt supplies

- revenue streams that are not part of taxable supplies/imports for threshold calculation

Step 4: Document your assumptions

If you rely on the “next 30 days” expectation test, keep proof:

- contracts and signed proposals

- purchase orders

- pipeline evidence and delivery schedules

- invoices or stage payment plans

This isn’t just internal discipline — it’s how you defend the decision if the facts are later questioned.

Real-world examples (so you can apply it quickly)

Example 1: Service business crosses AED 375,000

A Dubai-based consultancy has the following taxable billed amounts over the last 12 months:

- Months 1–9: AED 260,000

- Month 10: AED 45,000

- Month 11: AED 40,000

- Month 12: AED 55,000

Rolling 12-month total: AED 400,000

Result: Mandatory VAT registration applies. Waiting until “year end” is a mistake because the rolling calculation triggers earlier.

Example 2: Startup below AED 375,000 but spends heavily (voluntary registration)

A new trading business made AED 230,000 in taxable sales in the last 12 months (below the mandatory threshold), but has:

- significant inventory purchases,

- VAT invoices from UAE suppliers,

- and ongoing taxable expenses above the voluntary threshold criteria.

Result: Voluntary registration may be beneficial if recovering input VAT improves cash flow and the business can handle compliance.

Example 3: Non-resident business supplying into UAE

A foreign company provides taxable services into the UAE and invoices a UAE customer. Even if the annual value is below AED 375,000, VAT registration may still be required depending on who is responsible for settling VAT on that supply.

Result: Don’t rely on the AED 375,000 figure alone if you’re non-resident.

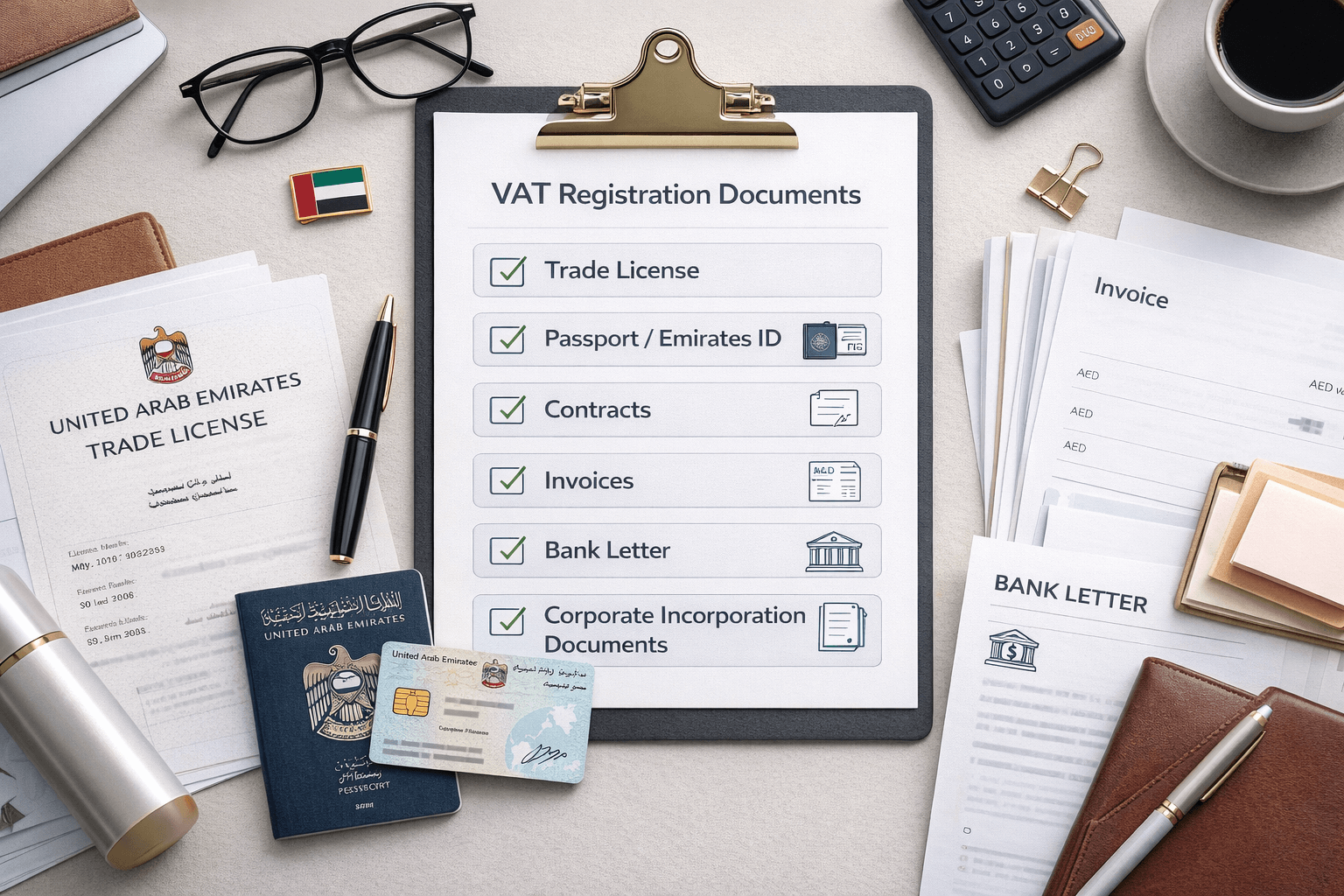

VAT registration UAE requirements: what you’ll typically need

VAT registration is done through the UAE’s tax platform and requires you to upload supporting documents and declarations.

Common requirements include:

- trade licence (and branch licences if applicable)

- incorporation documents (where applicable)

- passport and Emirates ID for owners and authorised signatories

- proof of authority for the signatory (where required)

- an official declaration of taxable supplies / sales figures to date

- evidence such as invoices, contracts, purchase orders, lease agreements, or completion certificates (depending on your business type)

- where registering based on expenses: VAT invoices supporting the level of taxable expenses

- customs information (if relevant)

- bank account details (sometimes optional, but recommended)

Fastest way to avoid delays: prepare your numbers and supporting evidence before you start the application. Most registration back-and-forth comes from unclear turnover figures or missing supporting documents.

Also see: UAE business setup support (licensing + compliance)

Step-by-step: how VAT registration works in practice

Here’s what a clean, low-friction registration path looks like:

- Create and activate your tax account

- Create the taxable person profile

- Start VAT registration

- Enter business activity details and ownership structure

- Provide turnover figures and threshold basis (mandatory vs voluntary)

- Upload supporting evidence (invoices, contracts, declarations, etc.)

- Submit and monitor for queries or requests for more information

- Once approved, download your VAT registration certificate and record your TRN

After you register: the obligations founders forget

VAT registration is not the finish line — it’s the start of ongoing compliance.

1) VAT invoices and TRN visibility

You must issue compliant tax invoices and ensure your TRN is used correctly.

2) VAT returns and payment deadlines

VAT returns and payments are typically due within a set number of days after the end of the tax period. Missing a filing deadline can trigger penalties.

3) Record keeping and audit readiness

Maintain VAT records in an orderly way and retain them for the required minimum period (and longer for certain special cases such as some real estate scenarios).

Operational tip: If your bookkeeping is messy, VAT will expose it quickly. A simple monthly close process (sales list, purchase list, VAT invoices, bank reconciliation) prevents painful quarter-end surprises.

Penalties for late VAT registration (and the hidden cost)

Late VAT registration is rarely “just a formality”. The two most expensive consequences are:

- Administrative penalties for failing to register on time

- Backdated VAT liability on taxable supplies made before you registered (which can reduce margins if you didn’t charge VAT on those invoices)

Even if your customers are businesses that could accept a VAT adjustment later, operationally it becomes harder to clean up once multiple invoices and payments are involved.

If you’re looking for an IFZA guide, check: IFZA company formation guide

A simple “VAT threshold check” you can do in 10 minutes

Use this quick checklist:

- I know which of my revenue streams are taxable, zero-rated, or exempt

- I can calculate taxable supplies/imports for the previous 12 months

- I have evidence for any “expected in next 30 days” threshold trigger

- I know whether my business is resident or non-resident for VAT purposes

- I have VAT invoices / contracts ready to upload if registering

- I’m prepared for ongoing VAT returns, invoicing, and record keeping

If you want this reviewed quickly, book a consultation with First Elite Global and we’ll confirm:

- whether you’re mandatory or voluntary,

- your likely effective registration date basis,

- and what documents you’ll need to submit cleanly the first time.

“First Elite Global handled everything for our Dubai consultancy licence. From activity selection to bank account coordination, it felt like having an in-house expansion team.”

Frequently asked questions

What is the UAE VAT registration threshold?

The mandatory UAE VAT registration threshold is AED 375,000 (based on taxable supplies and imports over the relevant time tests). The voluntary threshold is AED 187,500.

Is AED 375,000 based on revenue or profit?

It’s based on taxable supplies and imports (taxable turnover concepts), not profit. Some types of income may be exempt or treated differently, so it’s not always equal to total revenue.

What is the voluntary VAT registration threshold in the UAE?

Voluntary VAT registration becomes available once taxable supplies/imports (or certain taxable expenses) exceed AED 187,500 over the relevant time tests.

What is the VAT registration deadline after crossing AED 375,000?

Once you are required to register, you should submit the VAT registration application within 30 days of being required to register.

What documents are required for VAT registration in the UAE?

Common documents include trade licence, incorporation documents (if applicable), Emirates ID and passport for owners/signatories, proof of authority for signatory, declarations of taxable supplies, and supporting evidence such as invoices, contracts, purchase orders, and lease agreements.

Can a non-resident business register for VAT even if it is below AED 375,000?

Yes — non-resident VAT registration can be mandatory when making taxable supplies in the UAE depending on who is responsible for accounting for VAT on those supplies.

Helpful Links

- Federal Tax Authority — VAT Registration service page (requirements + documents)

- Federal Tax Authority — Registration for VAT overview

- Executive Regulation (VAT) PDF (thresholds + timing rules)

- Federal Tax Authority — Filing VAT Returns and making payments (return deadline basics)

- Ministry of Finance — VAT overview

- UAE official portal — VAT registration overview