If you’re looking to get an international FZCO, you’re usually trying to achieve three things at once: launch quickly, stay compliant, and build a company structure that banks and partners understand from day one.

This guide walks you through the full process, the decisions that shape your cost and timeline, and the practical details most “quick overview” pages skip. You’ll also get a bank-ready checklist, common delay triggers, and real-world examples to help you choose the right setup.

If you want a clear route plan tailored to your activity and budget, you can start here: book a free consultation with First Elite Global.

What an “International FZCO” is (and what it isn’t)

FZCO stands for Free Zone Company and typically refers to a multi-shareholder company registered in a UAE free zone. Many free zones use slightly different labels (e.g., FZCO, FZ-LLC, FZC), but the concept is similar: it’s a limited liability company licensed inside a free zone.

When people say “international FZCO,” they usually mean an FZCO designed for international business such as:

- Contracting with overseas clients

- Cross-border trading and distribution

- Holding IP or regional operations

- Hiring staff and sponsoring residence visas

- Invoicing in foreign currencies and building banking history

What it isn’t: a shortcut to unrestricted UAE mainland retail or government contracting. Mainland access depends on your activity, your licensing route, and how you plan to sell in the UAE.

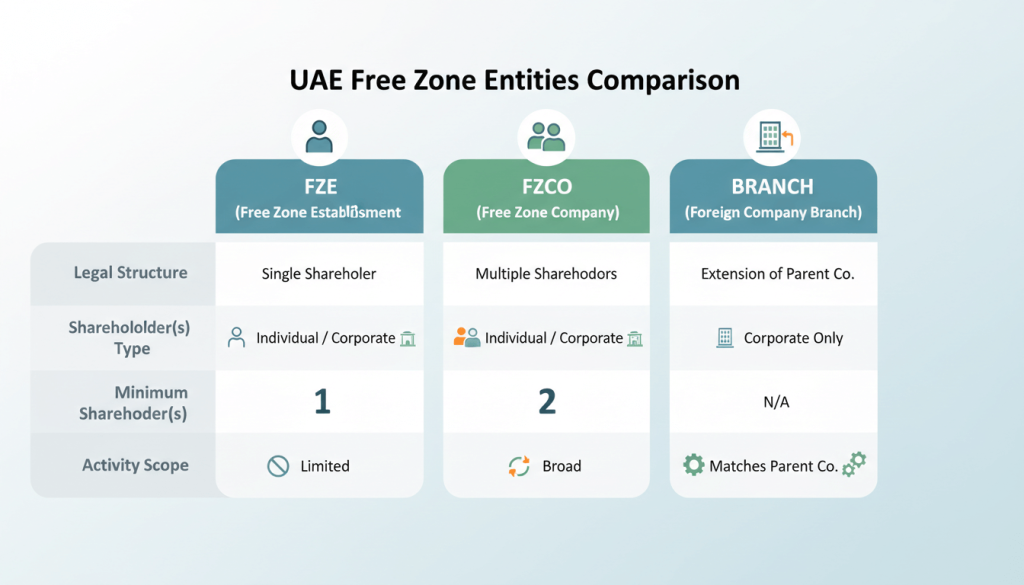

Free zone company types (choose the right one before you apply)

A strong application starts with choosing the right legal form. Here’s the simplest way to think about free zone company types:

| Company type | Best for | Typical shareholders | Key watch-outs |

| FZE | Solo founder setups | 1 | Adding partners later can require restructuring |

| FZCO | Partnered businesses and scalable ownership | 2+ | Shareholding structure must be clean and documented |

| Branch | Expanding an existing foreign/UAE company | N/A | Banking and approvals can be stricter; needs parent docs |

If your plan includes partners, investors, or bringing in shareholders later, FZCO is often the cleanest starting point.

To compare routes quickly (free zone vs mainland vs offshore), see: Company registration in UAE – free zone, mainland & offshore.

The 3 decisions that determine your cost, timeline, and approval odds

Before you submit anything, lock these in:

1) Your activity (what you’re licensed to do)

This drives:

- Which free zones can approve you

- Whether you need extra approvals (regulated activities)

- Your banking risk profile

Rule of thumb: pick the activity that matches how you’ll actually invoice and deliver work. “Close enough” activity choices can slow banking later.

2) Your jurisdiction (which free zone you choose)

Free zones vary dramatically in:

- Package pricing and renewals

- Visa allocation models

- Office/facility requirements

- Market perception for banking and counterparties

- Approved activity lists

If you’re still weighing free zone vs mainland, this is a helpful reference point: Business setup in Dubai.

3) Your ownership structure (how many shareholders and who they are)

A clean shareholding story improves approval speed and banking success. Make sure you can clearly show:

- Who owns what (and why)

- Where funds come from

- What the business will do in its first 6–12 months

If you want a setup built for partner ownership from day one, FZCO usually beats “start as FZE and change later.”

Step-by-step: how to get an International FZCO

Step 1: Define your “banking story” (yes, before licensing)

Most founders focus on licensing first and bank accounts later. Flip that:

- Who are your customers? (countries, industries)

- How do you get paid? (platforms, contracts, invoices)

- Where does initial capital come from?

- What will your first 3 transactions look like?

This single step reduces banking delays more than anything else in this guide.

If you’re planning banking early, you’ll also want this: Best bank for business account in UAE (guide).

Step 2: Choose the free zone and package (licence + facility)

Most free zones offer packages that combine:

- Licence issuance

- Facility (flexi-desk / shared / private office)

- Optional visa quota

Pick the package that matches your next 90 days, not your “future empire.” You can scale later, but over-buying visas and facilities upfront is one of the most common budget leaks.

Step 3: Reserve your trade name (and avoid rejection patterns)

Name rejection wastes time. Avoid:

- Restricted words (banking, government, authority, etc.)

- Overly generic names that resemble existing brands

- Missing legal endings where required

Have 3–5 options ready.

Step 4: Prepare your shareholder and manager document pack

For most international FZCO applications, you’ll typically need:

- Passport copies (shareholders + manager)

- Photo(s) meeting application requirements

- Entry status / visa status (if you’re already in the UAE)

- Contact details, addresses, and basic background info

- Company profile or brief business plan (especially for banking readiness)

For multi-shareholder FZCOs, expect additional ownership documentation.

Step 5: Submit the application and complete KYC

This is where most “mystery delays” happen.

Common KYC slowdowns include:

- Inconsistent addresses across documents

- Unclear source of funds

- Business activity that doesn’t match supporting materials

- Missing shareholder relationship explanation (for partner setups)

A well-prepared file moves faster and avoids back-and-forth.

Step 6: Sign incorporation documents and issue your licence

Once approved, you’ll sign the incorporation documents and receive your:

- Trade licence

- Company incorporation certificate

- Memorandum/Articles (format depends on free zone)

- Facility agreement/lease or desk allocation

Step 7: Set up visas (if needed) and Emirates ID

If you need residence visas for owners or staff, plan this immediately after licensing to avoid operational delays.

For broader visa support, see: UAE visa services.

Step 8: Open your business bank account (with a “bank-ready file”)

Banks want clarity, not complexity. Your bank-ready pack should include:

- Licence and incorporation documents

- Clear business model summary (1 page)

- Contracts or draft agreements (where possible)

- Website, professional email, company profile deck

- Expected monthly volumes and payment channels

- Source of funds explanation for initial deposits

Step 9: Build a basic compliance rhythm from day one

Even small companies should set:

- Accounting method and recordkeeping

- Invoice format and documentation

- Contract templates

- Owner resolutions and internal registers

This makes renewals, audits (if applicable), and bank reviews far easier later.

The International FZCO Document Checklist (copy/paste)

Use this list to reduce delays:

Core incorporation file

- 3–5 trade name options

- Final activity selection (with short description of how you’ll deliver it)

- Passport copies for all shareholders and the manager

- Proof of address (where requested)

- Shareholding breakdown (who owns what, % split)

- Brief business summary (what you sell, where, to whom)

Banking readiness file

- Company profile (1–2 pages)

- Website or landing page + professional email

- Draft contract / invoice template

- Source of funds statement (plain-English explanation)

- Expected transaction map (countries, currencies, payment methods)

Cost and timeline: what actually drives the numbers

Instead of chasing a single “FZCO cost,” focus on the levers that change the final price:

- Licence category (professional vs commercial vs specialist activities)

- Number of visas you need now (not later)

- Office requirement (flexi-desk vs dedicated office)

- Approvals for regulated activities

- Shareholder complexity (multi-country ownership, corporate shareholders, etc.)

- Banking support level (DIY vs guided bank-ready process)

A realistic planning approach is to define:

- Minimum viable setup (90 days)

- Growth setup (12 months)

- Scale setup (24 months)

If you want the clearest pricing path, start with a personalised plan: Contact First Elite Global.

Mainland access: how an International FZCO can sell in the UAE

Free zone companies are optimised for international operations and free zone-based activity. UAE mainland selling depends on:

- Your activity type

- Whether you need a local distribution arrangement

- Whether a dual-licence or additional approvals apply in your case

If mainland market access is central to your strategy, compare routes here: Dubai mainland business setup.

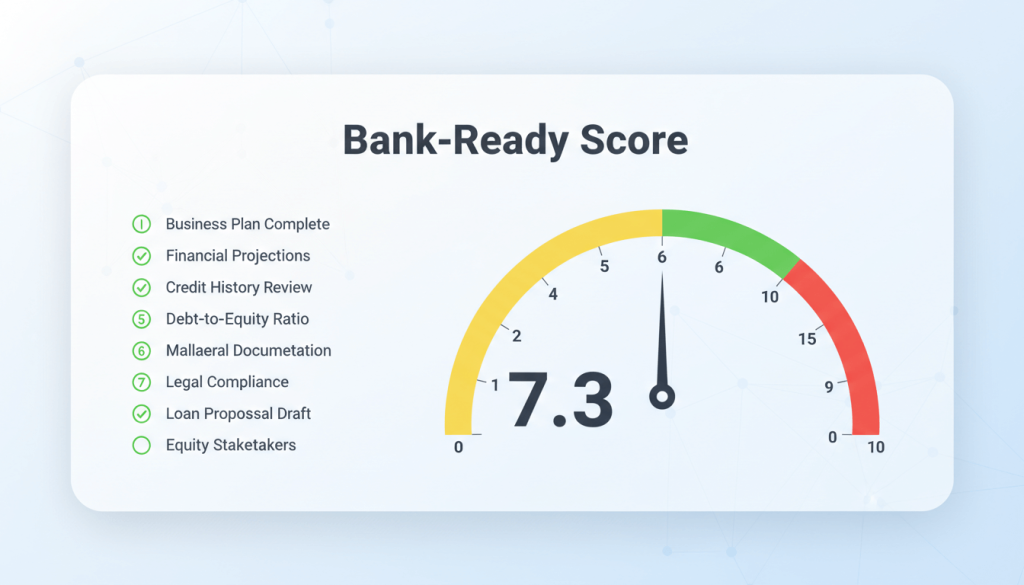

The Bank-Ready Score (original framework)

Most bank delays are predictable. Use this quick score before you apply:

Give yourself 1 point for each “Yes”:

- I can explain what we sell in one sentence.

- I have a clear customer profile (country + industry).

- I have a website or professional online presence.

- I have a professional domain email (not free webmail).

- I can show a draft contract or proposal.

- I can explain source of funds simply and document it.

- I know expected monthly volumes and currencies.

- I’m not relying on vague “general trading” unless it’s truly accurate.

- Shareholding is simple and easy to prove.

- I can show relevant experience (CV, portfolio, company history).

Score interpretation

- 8–10: strong bank readiness

- 5–7: workable, but expect questions

- 0–4: fix the story before you submit the application

If you want help turning your setup into a bank-ready file, speak with a consultant: Book your free consultation.

Compliance basics (keep it simple, keep it clean)

To run a healthy International FZCO long-term, treat compliance as a monthly habit, not a yearly panic.

At minimum, plan for:

- Corporate tax and filings (requirements vary by structure and activity)

- VAT considerations depending on your supplies and footprint

- Beneficial ownership and internal registers (as applicable)

- Accurate accounting records and clear invoicing

- Renewal timelines for licence, facility, and visas

If you want an end-to-end partner that keeps your file clean beyond licensing, First Elite Global can support company setup, visas, and ongoing PRO services: PRO services.

Common delays (and how to avoid them)

Delay trigger: activity mismatch

Fix: align activity, invoices, website wording, and customer story.

Delay trigger: unclear ownership or partner structure

Fix: provide a simple shareholding explanation and avoid complicated nominee arrangements.

Delay trigger: weak banking profile

Fix: prepare the bank-ready file early and keep your expected transaction volumes realistic.

Delay trigger: “general trading” without clear product scope

Fix: define what you trade, where you source, where you sell, and how you ship.

Delay trigger: poor documentation quality

Fix: clean scans, consistent data, and complete forms reduce rework.

Real-world examples (what setup fits what business)

Example 1: Two founders launching a consultancy (international clients)

Best fit: FZCO with professional activity

Why: clean partner ownership, simple invoicing, scalable visas later

Bank focus: contracts, portfolio, country exposure clarity

Example 2: Cross-border trading business (hardware or FMCG)

Best fit: FZCO with trading/commercial activity

Why: multi-shareholder structure supports procurement and operational roles

Bank focus: supplier docs, logistics flow, compliance on countries and products

Example 3: Startup with investor plans in 12–18 months

Best fit: FZCO from day one

Why: avoids later restructuring when shareholding changes

Bank focus: cap table clarity, funding story, audited statements where required later

Why founders choose First Elite Global for FZCO setup

When you’re trying to get an international FZCO, speed matters—but clean structure matters more. The difference between a smooth approval and months of friction is usually the quality of the file and the correctness of the route.

With First Elite Global, you get:

- A clear route recommendation (free zone vs mainland vs offshore)

- A streamlined document checklist tailored to your situation

- A bank-ready approach from day one (not as an afterthought)

- Visa and Emirates ID support when needed

- A single point of contact from plan to licence

“First Elite Global made setting up in Dubai surprisingly straightforward. They handled the paperwork, dealt with the free zone and bank, and kept us informed at every step.”

If you want a personalised setup plan you can act on immediately, start here: Contact First Elite Global.

FAQs

1) How do I get an international FZCO in the UAE?

To get an international FZCO, choose the right free zone and activity, prepare a clean shareholder document pack, complete KYC, issue the licence, then set up banking and (if needed) visas. The fastest path is the one with the fewest corrections—so prepare your bank-ready story before you apply.

2) What’s the difference between FZCO and FZE?

FZE is usually a single-shareholder free zone company. FZCO is typically a multi-shareholder free zone company. If you have partners now (or will soon), FZCO often avoids future restructuring.

3) Can an international FZCO sell in the UAE mainland?

Sometimes—depending on your activity and route. Many free zone companies focus on international business and free zone operations. Mainland selling may require additional arrangements or approvals. If mainland access is central, consider a mainland route or a hybrid strategy.

4) How long does FZCO setup take?

Timelines vary by free zone, activity approvals, and file quality. The biggest time-saver is submitting a complete application and preparing banking documentation early so your company can operate immediately after licensing.

5) Do I need an office to set up an international FZCO?

Most free zones require some form of facility solution (which may be a flexi-desk or shared office depending on package). The “right” option depends on visa needs and how you operate.

6) What documents do banks usually ask for after FZCO formation?

Banks commonly request the licence and incorporation documents, a clear company profile, website and domain email, expected transaction details (countries/currencies), and source of funds information. A prepared bank-ready pack significantly reduces delays.